Oddbean new post about login | logout

Oddbean new post about login | logout MicroStrategy's bitcoin acquisition strategy has been really on-point. I analyze a lot of stocks and see how they manage their shares. Most companies are rather pro-cyclical in this aspect. They buy back a lot of shares when times are good and shares are expensive, and then when there's a recession they reduce or eliminate their share repurchases, ironically when shares are cheap and it would be better to buy them. A small percentage of companies have more forward-thinking executives that manage to do this more counter-cyclically. They buy back more shares then they are cheap, and they retain more cash or do other things with their cash when their shares are more expensive. MicroStrategy has been doing this quite well, except it's about the strategy of issuing shares for bitcoin, which if bitcoin continues to be successful will have more impact overall. When MicroStrategy wants to buy more bitcoin (which is always), what they seem to be optimizing for is how many bitcoin can they get per share. That's what builds shareholder value in this context. So when MicroStrategy stock is trading at a valuation premium relative to its underlying bitcoin, they can take that opportunity to issue more of these expensive shares, and buy bitcoin with those proceeds. When there is not a valuation premium, they can focus more on just buying bitcoin with incoming cash flow, or exploring other low-cost financing. So far, they have been really on-point about managing this. https://m.primal.net/HRjg.png

Thanks for elaborating on this!

No surprise that you get it too! I feel I’m in good company. https://damus.io/note1fw3nlsj6fyj7gxz4pqk4u2gwqzq2u8kvq88d37kcwk6hnndj2zksld99nt

But wouldn't that put shareholder value at "risk"? and I'm just talking from a business model/growth type of risk...selling shares and the consequent increase in value is more biased towards the underly digital asset as opposed to better / more competitive tech (MSTR products and services) and consequently better cashflow? So while MSTR may increase SVA in the short run the longevity of the business would be at risk in the long run?

My response is based on what I’ve heard Saylor say regarding the subject, but basically it boils down to this: They can’t compete with their competitors like Oracle and IBM when it comes to R&D spend, or employee acquisition/retention based on their primary business model of enterprise software. Essentially they were a business doomed to fail prior to the bitcoin treasury strategy. By adopting bitcoin as a treasury reserve asset, they have a way to preserve their cash flows in an instrument that will appreciate against the value of their cashflows, which will increase their equity value, allowing them to sell more shares to fund whatever they want to fund, which seems to primarily be buying more bitcoin. Now, you’re right in that there is shareholder dilution, but the goal is to have the bitcoin acquisition increase the value of the company more than the shares are diluted, similar to the acquisition of a business which provides more value to shareholders than the opportunity cost of acquiring that company, I.e. his goal is to make the purchase in of bitcoin an accretive endeavor for shareholders. So far, this has been the case. He has essentially positioned the company to be a bitcoin investment vehicle more so than an enterprise software company. Institutional investors that can’t buy bitcoin can buy microstrategy stock and therefor get leveraged exposure to the underlying asset. They just take on counterparty risk regarding how microstrategy custodies their bitcoin. But essentially, they’re a leveraged bitcoin etf that has underlying cash flow from an enterprise software company rather than charging a management fee like a traditional ETF would.

A future unclear question in my mind is, if their MacroStrategy (as they’ve branded it) pans out and they 10-20x their market cap, would they scale the core business or do M&A in order to grab market share from the bigger data-analytics companies? Or is it a situation where it’s a fun trivia fact years from now, that this bitcoin holding company started as a small enterprise data company, like how Berkshire started as a small textile company?

Of those two scenarios, likely the latter. Although I think if they were looking to spend more money on improving their cash flows, they wouldn’t try to take market share from their competitors in enterprise software but rather look to carve out a niche in providing enterprise-oriented bitcoin solutions, layer 3 work, web5 work with @jack etc. I don’t see them as being interested in trying to overtake IBM and Oracle, but rather being the Bitcoin enterprise software company. That’s their win condition, from a cash flow perspective

Yeah, I think that’s spot on.

Not to mention they’re frontrunning banks and the giant tech companies with their balance sheet. Bitcoin either gets attacked by government or it doesn’t. If it doesn’t get attacked, then the accumulation done by companies like apple Google meta Nvidia etc combined with the large banks will give them one of the largest debt-to-equity ratios in the US market. If the government does try to attack bitcoin, either via harmful regulation or attempted seizure, we’ll see how it plays out on whether the govt will actually get the bitcoin, or if Saylor tries to hop ship, burns the keys, etc etc. Uncharted waters in this scenario.

Ya it's bc they also got in on a high price of BTC right ? So they feel like they have to make up ground.

No one uses #Bitcoin more intelligently than Michael #Saylor of #MicroStrategy..👏👍🧡😊

Your post is getting a lot of attention. Added to the https://nostraco.in/hot feed

I have been thinking about MSTR stock performance vs BTC etf . Over time the only way MSTr can outperform the ETF is when the company cash flow is growing faster than the BTC etf . I am making some assumptions , the value of BTC on books is reflected in stock price . As this value dwarfs the rest of the co value , the stock performance of MSTR will approach ETF performance Any thoughts, anyone?

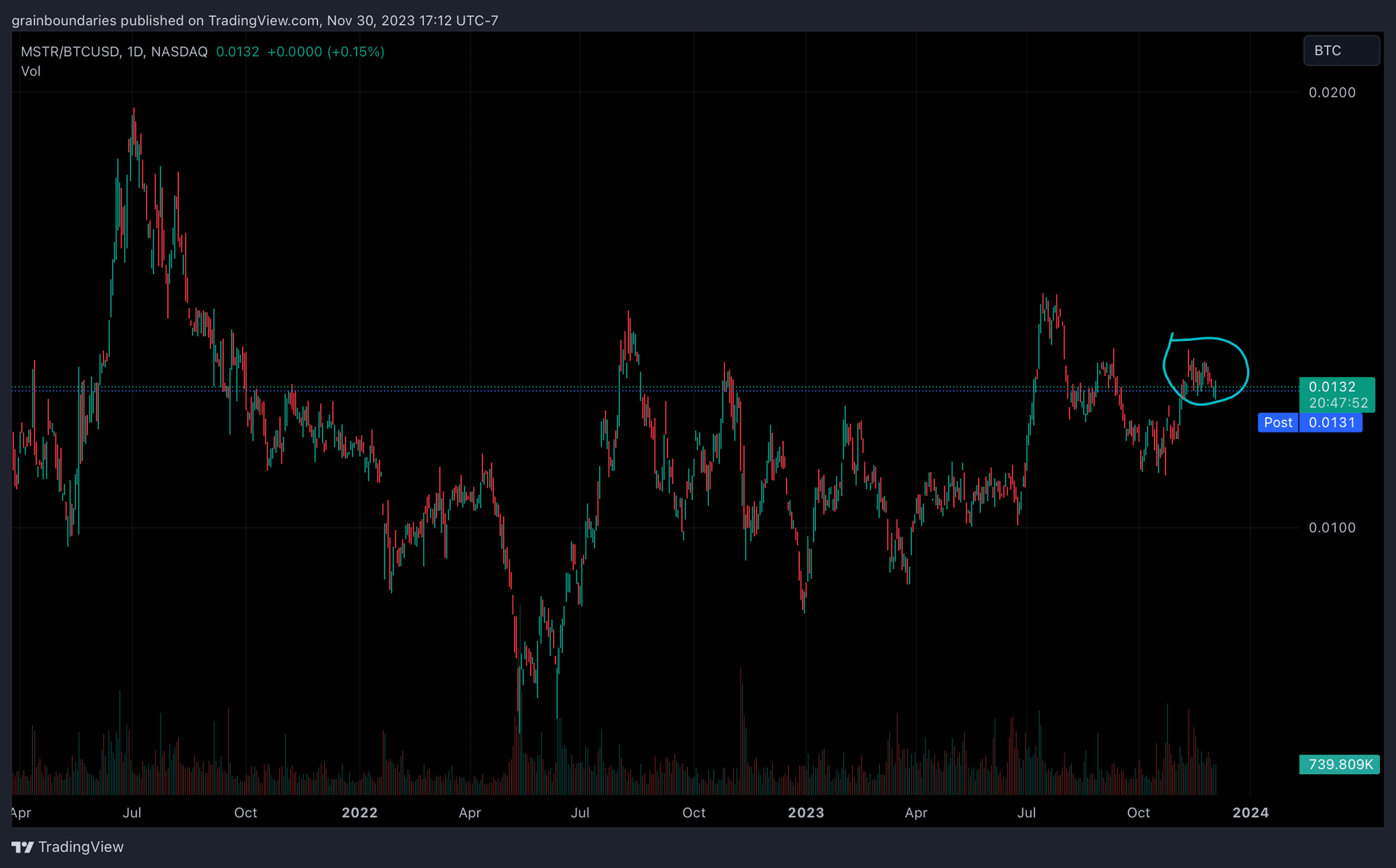

The recent purchase was conducted over the course of November, see blue circle. This clearly lines up with a local above-average ‘peak’ when viewed as Microstrategy stock denominated in Bitcoin (MSTR/BTCUSD). They will continue to do this whenever the market values their stock more. This sanity will persist as long as the fiat denominated world remains deluded in their insanity. https://image.nostr.build/ea130a2de083535de81da8a99d6f388e20f0a34cc4f45f241e4fe3bddf5bb33a.png

Hey Lyn, I realize MSTR doesn't charge management fees like an ETF will, plus they use leverage that's not marked to market, giving them a potential advantage over ETFs. Nonetheless, I'm concerned that the demand for MSTR will decline upon approval of an ETF bc I believe some people will just want to own the asset and avoid potential complications that may arise from owning a stock that owns the desired asset. What do you expect for MSTR? If you want to cover that in your subscription service, I would be pleased to read about it. Thank you!

@preston called this MacroChadegy and that might be my new favorite term

{kind=link}

{kind=link}

{kind=link}