Oddbean new post about login | logout

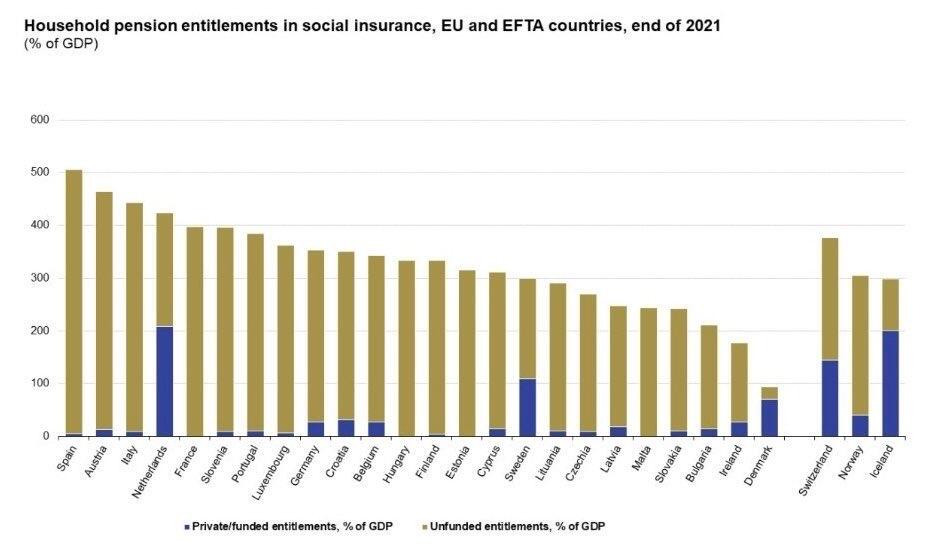

Oddbean new post about login | logout The scale of the unfunded pension liabilities globally is almost incomprehensible. Hundreds of millions of people around the world expecting to retire comfortably will see their pensions worth pennies on the dollar or their currencies completely debased. https://image.nostr.build/21e54a608c833f3d20339a5bf8752ad5f2b9177b7fed0a783b59e672907a2456.jpg

I think about this every paycheck, when I see the amount of money being taken from me to go to support someone else in their retirement. The promise is that I'll likewise be supported by others in the same way in my old age. I fear the reality is that I will never see the money again.

My generation will be lucky if the pension we get can afford a loaf of bread (I'm from Spain). When I tell people to save and invest to have a plan B since the public pensions are unsustainable in the medium to long term they refuse to believe it. We can't kick the can down the road forever... but people are so statist and socialist here that they think government will fix all their problems. Sad.

The source please!?

79% funded according to recent reports https://www.plansponsor.com/funded-status-of-the-largest-public-pension-funds-rises/

Good times

In fiat, the average joe props up the system with THEIR time & energy thru usury-debt servitude. The citizen is the human-miner reaping empty promises of future reward. But..there is no pension. In Bitcoin, work is transfer over to miner-machines freeing the human to enjoy the present.. or at most a lag of 8-12 years until they can feel economically safe.

you have no idea how many in my office sacrifice their salaries ( proof of slavery ) into pension funds. 99.9% of them do. i am the only one all in into #bitcoin and they tell me i am crazy 🤪 😜 🙃 😅

I moved jobs 5 years ago to get all my 401k and turn it into bitcoin. Did not start a new retirement plan at new job despite a ‘good’ company match. Bitcoin has much better control and return.

yes as long as you control your keys and be extra careful in protecting them

Yep, at least now, I'm sort of paying my parents' pensions, but after that...

That's one hell of a chart. It's almost as though it's been extracted.

Here in Finland, employees contribute 7-9% of their salary to "pension funds" and employers contribute 17-18%. That's 25% of the salary into this disastrous ponzi scheme. Everyone knows they are royally screwed, yet they do nothing. The government just sneakily raises the retirement age by 3 months here and there...

And people are laughing at me when i tell them that me and my peers are not going to get any retirement money ...

they receive an amount X but the purchasing power will hardly be available any more

Amount of X worth of nothing is still nothing, init ?

I think Switzerland and Norway will have a much smaller problem with this than Spain and Italy 😅

Denmark seems unusually good; not crossing total GDP, and lowest proportion of unfunded liability. What are they doing differently?

I see a future of smaller "Family Offices" where a pleb-fam tithes to their own pension (guess what in) and their decedents only gain access to the family pension (aka Living Trust - See Kennedy Family Trust) by tithing to it themselves (covenants). After a couple of generations the Family Pension generates enough income to support the basic needs of the decedents without any intervention or 3rd party custody by institutions or governments. Do you want more? Then do the thing that makes more. Make more? Tithe more. Our 401k has tricked us into believing we aren't capable of such machinations and that serves the purposes of only those who do not care about you, your family or your legacy. #bitcoin #lightningNetwork #nostr #keyPairs #relays #Ecash The components are here and it's time to build the thing. nostr:note1dg8sn4vm4wmyw2alv0s8weuvgw6pvernpgdqaugl6g4zsgghsalqxp96gd

_________.

#Mandibles !

Where does the USA fall on this chart?

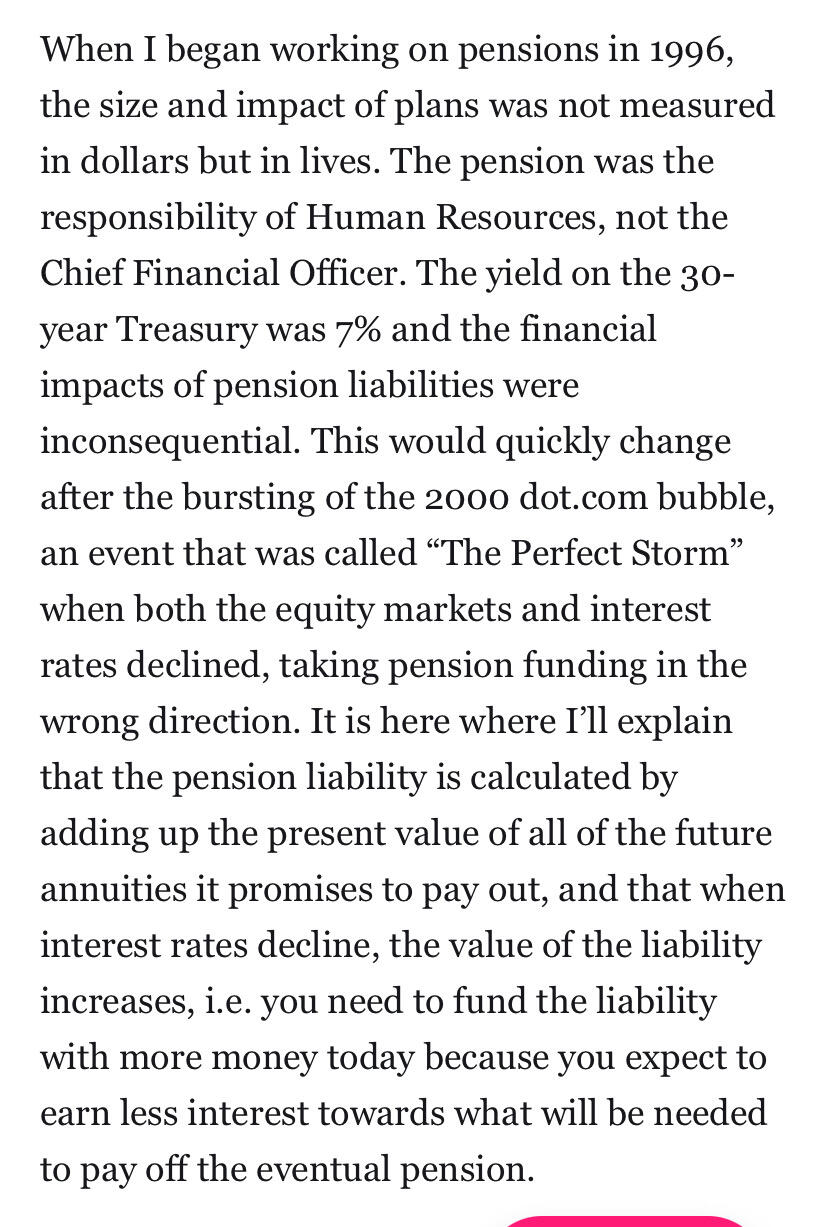

This subject is too loaded for this platform but I’ll leave a few bytes to chew on: 1. The unfunded pension liability in the US is over $200T which puts us over 600% - IF AND ONLY IF you believe the assumptions 2. Don’t believe the assumptions. I’m an actuary and used to set these assumptions. I quit pensions because of how corrupt this process was and I didn’t want to be part of the implosion with my signature on any of it. Example: Most of the big state plans claim they are well funded because they assume discount rates equal to the expected return of the assets. So even when rates are at local maximums like they are now, they are far below the 7 or 8% the big state plans like CALPERS are using - this makes the liabilities look a lot lighter than they actually are. The 200T might be 400T just if we use a more realistic discount rate for the future claims. Here’s a little essay I wrote after the BoE bailout to try and explain some of this https://risk-fundamentals.ghost.io/pensions-finally-come-of-age/

{kind=link}

{kind=link}