Target Shares Crash On Profit Miss, Downgraded Outlook, & Market Share Loss As Walmart Reigns Supreme

Target Shares Crash On Profit Miss, Downgraded Outlook, & Market Share Loss As Walmart Reigns Supreme

The current consumer environment is very dire for households making less than $100k a year, with the surge in the trade-down phenomenon—driven by both wealthy and low-income consumers grappling with record credit card debt and sliding personal savings—solidifying https://www.zerohedge.com/markets/walmart-beats-lifts-outlook-3rd-time-increasingly-more-wealthy-americans-trade-down-big-box

as 'America's low-cost budget retailer,' quickly eroding market share from competitors like Target and Dollar General into the end of the year.

Target https://corporate.target.com/press/release/2024/11/target-corporation-reports-third-quarter-earnings

a disappointing margin performance for the fiscal third quarter on Wednseday and slashed the annual EPS forecast over market share losses.

It reported higher digital fulfillment and supply chain costs, resulting from elevated inventory levels and increased digital sales volumes.

"We saw several strengths across the business, including a 2.4% increase in traffic, nearly 11% growth in the digital channel, and continued growth in beauty and frequency categories," Chief Executive Brian Cornell wrote in a statement, adding, "We encountered some unique challenges and cost pressures that impacted our bottom-line performance."

Here's a snapshot of third-quarter results (courtesy of Bloomberg):

Comparable sales +0.3% vs. -4.9% y/y, estimate +1.48%

Comp digital sales +10.8%, estimate +4.69%

Sales $25.23 billion, +0.9% y/y, estimate $25.74 billion

Gross margin 27.2%, estimate 28.7%

Ebit $1.20 billion, -11% y/y

Ebitda $1.95 billion, -5.5% y/y, estimate $2.16 billion

Customer transactions +2.4%

Average transaction amount -2%, estimate -1.08%

Digital sales as share of total sales 18.5%

Total stores 1,978, estimate 1,972

Operating margin 4.6%, estimate 5.63%

Store comparable sales -1.9%, estimate +1.49%

Stores originated sales 81.5%, estimate 82.7%

Adjusted EPS $1.85 vs. $2.10 y/y, estimate $2.30

Operating income $1.17 billion, -11% y/y, estimate $1.46 billion

Target expects fourth-quarter adjusted EPS of $1.85 to $2.45, versus the current Bloomberg Consensus of $2.65

Sees adjusted EPS $1.85 to $2.45, estimate $2.65

Several months after Target executives raised financial targets, these rosy outlooks have reversed into the holiday shopping season amid weak consumer trends:

Sees adjusted EPS $8.30 to $8.90, saw $9 to $9.70, estimate $9.57 (Bloomberg Consensus)

"It's disappointing that a deceleration and discretionary demand combined with some cost pressures have caused us to take our guidance back down after raising it last quarter," Michael Fiddelke, Target's chief operating officer and former chief financial officer, told investors on the earnings call, adding, "We believe it's prudent to take this conservative approach."

The quarter's dismal earnings and revised outlook spooked investors, prompting some to question whether Walmart's 'rollback deals' are eroding Target's market share in the consumer space.

Target shares crashed 18% in premarket trading in New York.

https://cms.zerohedge.com/s3/files/inline-images/2024-11-20_09-18-41.png?itok=P_E80FQP

Commenting on Target's earnings report, Goldman's Eric Mihelc and Scott Feiler told clients this morning:

TGT (-18%) the clear focus this morning which is weighing on other general merch names too (DG, FIVE, DLTR -3%)...though it's not all bad for consumer; witness WMT comps +5% yest, DAL saying premium consumer is 'thriving' and TJX +0.5% on earnings this morning. Some helpful takeaways from Scott here: link. Elsewhere, GIR updates MF and HF positioning post 13F filings. Most active high touch yesterday: UAA, CELH, SKX, KHC, WMT, AS, WRBY, FND, GIS, SBUX, MLCO, KO, CCL, GAP, KMB.

The analysts continued:

TGT -20%...Expectations were muted, which is why short interest was near 4 year highs. However, the low bar was on the comp sales, which were not much worse vs expectations. Bar was not low for a big EPS issue, which they ended up having one. Gross margins 100 bps light for 3Q and 4Q margins are also implied to be well below. The stock is down 20% in the premarket on an 8% FY EPS cut, so it does feel extreme. Having said that, almost nobody I spoke to had this big of an earnings miss/cut as their base expectation. Details: 3Q EPS of $1.85 vs Consensus $2.30 on comp sales +0.3% vs Consensus +1.5% (we think bogey was +0.5%). The issue of course is EPS/margins miss, with gross margins 130 bps light (SG&A was in-line, so gross margin drove all the downside). 4Q EPS well below at $2.15 (mid) vs Consensus $2.65 on comps of flat vs Consensus +1.3%.

Peer read? TGT did have +2.4% traffic growth vs +3% last quarter, so traffic is ok. As a result, Scott does not think all of Retail needs to get aggressively sold. However, when a name like TGT is down 20% and has 60% discretionary exposure, the natural reaction will be for other discretionary general merchandise names to see some underperformance. Would expect an elevated focus on DLTR, DG, FIVE, TJX (reports this morning also), ROST, BURL, etc...

On a separate note, Goldman's Feiler explained to clients that the current consumer environment is a "winner-take-all" situation. So far, Walmart appears to be the king of deals (see: latest https://www.zerohedge.com/markets/walmart-beats-lifts-outlook-3rd-time-increasingly-more-wealthy-americans-trade-down-big-box

), and cash-strapped consumers are responding to deals by flooding the big box retailer's stores nationwide.

Here are Feiler's six points on the current consumer environment:

Takeaway # 1: We are in a Consumer environment that is steady enough that winners can continue to outperform (see WMT yesterday with +5.3% Walmart US comp sales and stock was +3% to new all-time highs, despite the elevated multiple to history).

Takeaway #2: However, we are not in a Consumer environment that is good enough that it is a rising tide lifts all boats. There will be winners (WMT) and there will be share donors (see TGT this morning).

Takeaway #3: Dispersion is the name of the game and the current consumer environment supports a winners/losers environment. I would expect that to continue into the rest of EPS season and 1H25. We are seeing it in COST/WMT vs TGT. We are likely to see it in grocers and big box discounters vs dollar stores. We have seen it in footwear with ONON/DECK vs NKE, in MCD vs peers and in many other end markets as well.

What Happened This Morning?: TGT is down 20% in the premarket. Expectations were muted, which is why short interest was near 4 year highs. However, the low bar was on the comp sales line, which was not much worse vs expectations (+0.3% vs Consensus +1.5% and the bogey for +0.5%). The bar was not for a big EPS issue, which ended up being the big surprise here($1.85 vs Consensus $2.30). Gross margins are 100 bps light for 3Q and 4Q margins are also implied to be well below.

What to Do Here? The stock is down 20% in the premarket on an 8% FY EPS cut, so we are seeing some further multiple compression, despite 4-year high short interest. Having said that, almost nobody I spoke to had this big of an earnings miss/cut as their base expectation. I would expect to see some short covers, but do not think long buyers will be quick to step in and take a more constructive view.

Peer read? TGT did have +2.4% traffic growth vs +3% last quarter, so traffic is ok. As a result, I do not think all of Retail needs to get aggressively sold. However, when a name like TGT is down 20% and has 60% discretionary exposure, the natural reaction will be for other discretionary general merchandise names to see some underperformance. Would expect an elevated focus on DLTR, DG, FIVE, TJX (reports this morning also), ROST, BURL, etc.

Other Wall Street analysts offered their take on TGT ER (courtesy of Bloomberg):

Citi (neutral from buy, PT $130 from $188), Paul Lejuez

"Very poor" 3Q results and an "uninspiring" 4Q outlook show Target is probably losing market share to Walmart, Lejuez writes

With Walmart's share gains coming "largely from higher income consumers," Target is at risk of losing additional share

"We believe TGT is likely to need to be more promotional to drive traffic/sales, which we believe makes F25 much more uncertain, especially because in 3Q TGT did not show an ability to adjust SG&A to offset the sales/gross margin weakness," he says

Oppenheimer (outperform), Rupesh Parikh

Parikh said in his Target earnings preview note that he expected comparable sales and earnings for 3Q to show a "material" shortfall compared with Street estimates, but the actual bottom line miss is even "deeper" than he anticipated

Awaits the conference call to "better understand margin dynamics for the balance of the year and into FY25"

The stock pullback this morning is "much greater" than the possible downside in the mid-$130s/low $140s he envisaged with the preview note

Stifel (hold), Mark Astrachan

"We view results as disappointing, with comp. [sales] worsening sequentially y/y and on a 2-year basis," Astrachan writes

This suggests that Target is underperforming compared with larger peers, and is losing market share in key categories, which probably is also hurting gross margin

Expects shares to decline by more than the anticipated ~10% reduction in the annual consensus EPS

Bernstein (market perform), Zhihan Ma

"Disappointing quarter calls Target's ability to generate profitable growth into question," Ma writes, adding that she wonders if the company can "exceed both sales and profitability expectations at the same time over the long term"

Target needs to invest in pricing and drive e-commerce growth to support top-line growth, but both of these actions are "margin dilutive"

She believes Target is less likely to turn profitable in e- commerce than Walmart due to its "smaller scale and limited investment in automated e-commerce fulfillment capabilities"

RBC (outperform), Steven Shemesh

"The conclusion investors seem to be drawing is that there aren't a ton of margin levers left to pull if top line remains on the weaker side throughout 2025," Shemesh writes

"Back of the envelope math suggests that ~flat to +1% comp in 2025 and ~flat op margin would yield EPS around $9.50, which at ~15x gets us to somewhere around $140-145, roughly ~10% upside from where shares are trading pre-market ($128)"

Premarket share reaction (down around 18%) probably fades throughout the day, but with visibility into a sales recovery limited, he wouldn't advise shorter-term investors to chase the stock here

For longer-term investors, $10.50-$11.00 in EPS seems achievable in 2026

Vital Knowledge, Adam Crisafulli

"This weak TGT print underscores how a big part of Walmart's strength is market share gains while the consumer overall continues to witness headwinds," Crisafulli writes

Results likely don't bode well for the likes of Kohl's and the dollar stores

Considering the current challenging consumer environment...

https://cms.zerohedge.com/s3/files/inline-images/savings%20rate%20revised%20vs%20credit%20card.jpg?itok=h9P4o7fD

...let's remember that in July, we cited Goldman as saying...

Attention Cash-Strapped Americans: Goldman Finds Top Supermarket Offering The Best Grocery Deals https://t.co/0WSTOWex5J

— zerohedge (@zerohedge) https://twitter.com/zerohedge/status/1802029588479885425?ref_src=twsrc%5Etfw

And in October.

Walmart Wins: Best Grocery Deals Out There!

👉 Walmart offers groceries 14% cheaper than average, per Goldman analysts.

👉 Whole Foods is the priciest, with +10.1% compared to peers.

👉 Dairy deal alert: Walmart at -18.1%, while Whole Foods' prices soar +11.3%.

‼️ Economically… https://t.co/CgB0nImpXP

— ZeroHedge Notes (@ZeroHedgeNotes) https://twitter.com/ZeroHedgeNotes/status/1849405346831303090?ref_src=twsrc%5Etfw

A more recent note by Goldman analysts found the "https://www.zerohedge.com/markets/goldman-finds-trade-down-phenomenon-strikes-rich-poor-consumers

" has occurred across "high-end and low-end consumers."

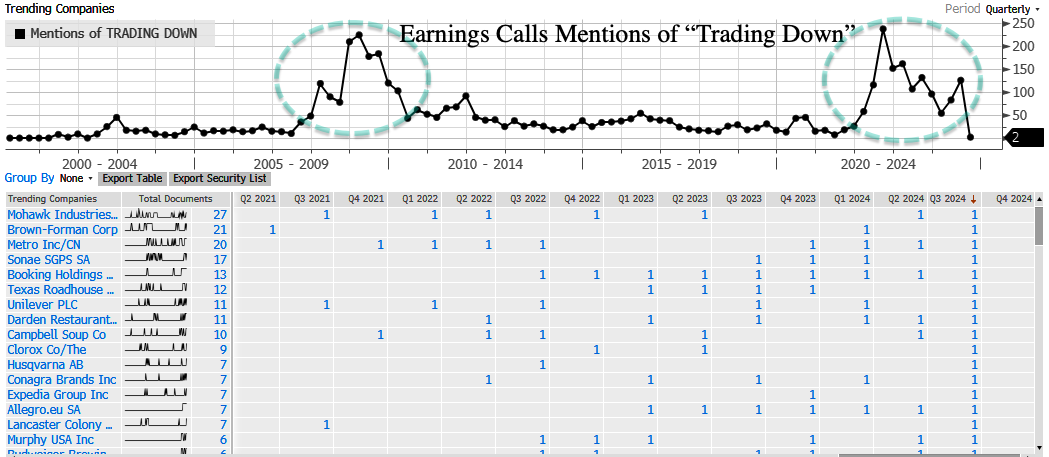

The last time "https://www.zerohedge.com/markets/earnings-call-mentions-consumer-downturn-soar-highest-level-financial-crisis

" mentions spiked on earnings calls, it was GFC.

https://cms.zerohedge.com/s3/files/inline-images/Snag_cf04efd.png?itok=2ByGF4BS

Bidenomics has transformed American households into a nation of Walmart customers ...

https://cms.zerohedge.com/users/tyler-durden

Wed, 11/20/2024 - 09:25

https://www.zerohedge.com/markets/target-shares-crash-profit-miss-downgraded-outlook-market-share-loss-walmart-reigns-supreme  Oddbean new post about login | logout

Oddbean new post about login | logout {kind=link}

{kind=link}

{kind=link}